Globalisation has led to an increase in votes for the political fringes in Europe. A study by the Halle Institute is the first to show the long-term consequences of increased Chinese imports in European regions: far-right and populist parties in particular have benefited from the so-called China shock in national elections.

Headwinds from Germany and abroad: institutes revise forecast significantly downwards

According to Germany’s five leading economic research institutes, the country’s economy shows cyclical and structural weaknesses. In their spring report, they revised their GDP forecast for the current year significantly downward to 0.1%. In the recent fall report, the figure was still 1.3%.

The IWH comes fourth in the institute ranking of the “Forschungsmonitoring 2023” taking into account A and A+ publications, and also on a per capita basis. This puts the IWH ahead of all other economic research institutes in the Leibniz Association. The ranking is compiled by the KOF Swiss Economic Institute at ETH Zurich. It evaluates the publication performance of economists and research institutions in German-speaking countries.

Risk in the financial sector: close ties between banks and supervisors

Many top managers at European banks move seamlessly to their supervisory authorities. An IWH study has revealed the extent of these personnel links for the first time. They can pave the way for lax regulation and jeopardise financial stability. Three things politicians should improve.

If a senior executive refuses to give information to professional investors, the company's stock market value drops afterwards. This is shown in an IWH study after evaluating 1.2 million answers from telephone conferences.

Exclusively for non-commercial scientific purposes, the IWH European Real Estate Index (EREI) provides a comprehensive overview of residential property offers for sale and rent in 18 European countries.

We provide independent research on economic topics that really matter and aim to enrich society with facts and evidence-based insights that facilitate better economic decisions. We focus on growth and productivity because we are convinced that economic prosperity enables people to lead happier lives. We provide young researchers a nurturing place to develop their competencies and to make the most of their skills. Working in flat hierarchies, we are driven by open-minded intellectual curiosity and we have the courage to share inconvenient insights.

Globalisation has led to an increase in votes for the political fringes in Europe. A study by the Halle Institute for Economic Research (IWH) is the first to show the long-term consequences of increased Chinese imports in European regions: Far-right and populist parties in particular have benefited from the so-called China shock in national elections.

IWH-Insolvenztrend: Zahl der Firmenpleiten im März abermals auf Rekordniveau

Professor Dr Steffen Müller

Abstract

Die Zahl der Insolvenzen von Personen- und Kapitalgesellschaften ist im März auf einen weiteren Höchstwert gestiegen. Nie seit Beginn der Erhebung durch das Leibniz-Institut für Wirtschaftsforschung Halle (IWH) im Januar 2016 gab es mehr Firmenpleiten. Allerdings ist ein Ende des Anstiegs der Insolvenzzahlen in Sicht.

East Germany's lead over West Germany in terms of growth is bound to shrink – Implications of the Joint Economic Forecast Spring 2024 for the East German economy

Professor Dr Oliver Holtemöller

Abstract

In 2023, the East German economy is expected to have expanded by 0.5%, while it shrank by 0.3% in Germany as a whole. The Halle Institute for Economic Research (IWH) forecasts an East German growth rate of 0.5% again for 2024, and a rate of 1.5% in 2025. The unemployment rate is expected to be 7.3% in 2024 and 7.1% in the following year.

Joint Economic Forecast 1/2024: Headwinds from Germany and abroad: institutes revise forecast significantly downwards

Professor Dr Oliver Holtemöller

Abstract

According to Germany’s five leading economic research institutes, the country’s economy shows cyclical and structural weaknesses. In their spring report, they revised their GDP forecast for the current year significantly downward to 0.1%. In the recent fall report, the figure was still 1.3%. Expectations for the coming year are almost unchanged at 1.4% (previously 1.5%). However, the level of economic activity will then be over 30 billion euros lower due to the current weak phase.

in: Journal of Money, Credit and Banking,

forthcoming

Abstract

Abstract This paper investigates the relationship between heterogeneity in sectoral price stickiness and the response of the economy to aggregate real shocks. We show that sectoral heterogeneity reduces inflation persistence for a constant average duration of price spells, and that inflation persistence can fall despite duration increases associated with increases in heterogeneity. We also find that sectoral heterogeneity reduces the persistence and volatility of interest rate and output gap for a constant price spells duration, while the qualitative impact on inflation volatility tends to be positive. A relevant policy implication is that neglecting price stickiness heterogeneity can impair the economic dynamics assessment.

in: Journal of Financial and Quantitative Analysis,

forthcoming

Abstract

Mutual fund families increasingly hold bonds and stocks from the same firm. We present evidence that dual ownership allows firms to increase valuable investments and refinance by issuing bonds with lower yields and fewer restrictive covenants, especially when firms face financial distress. Dual holders also prevent overinvestment by firms with entrenched managers. Overall, our results suggest that mutual fund families internalize the agency conflicts of their portfolio companies, highlighting the positive governance externalities of intra-family cooperation.

in: Jahrbücher für Nationalökonomie und Statistik,

forthcoming

Abstract

Using a newly collected dataset at the plant level from 2014 to 2018, we provide the first microscopic portrait of robotization in Germany and study the correlates of robot adoption. Our descriptive analysis uncovers five stylized facts: (1) Robot use is relatively rare. (2) The distribution of robots is highly skewed. (3) New robot adopters contribute substantially to the recent robotization. (4) Robot users are exceptional. (5) Heterogeneity in robot types matters. Our regression results further suggest plant size, high-skilled labor share, exporter status, and labor shortage to be strongly associated with the future probability of robot adoption.

in: Journal of Business Finance and Accounting,

forthcoming

Abstract

Abstract This paper investigates how state ownership affects financial reporting practices in China. Using several measures of state (government) ownership, we show that a one-standard-deviation increase in state ownership decreases financial statement comparability by 36.61%, and the impact is more pronounced when the central authority has majority control of the company. Moreover, lower earnings quality and lower levels of accounting conservatism among state-owned enterprises (SOEs) may explain the lower accounting comparability between SOEs and non-SOEs (NSOEs). Additionally, similar (different) managerial objectives converge (diverge) financial statement comparability between SOEs and NSOEs. Last, the geographical locations of firms also contribute to financial statement comparability. We employ a difference-in-differences design, changes regression and entropy balancing to mitigate potential endogeneity bias.

in: Journal of Business Finance and Accounting,

forthcoming

Abstract

Abstract This paper investigates a firm's stock return asynchronicity through the auditor's perspective to distinguish whether this asynchronicity can proxy for the company's firm-specific information or the quality of its information environment. We find a significant and positive association between asynchronicity and audit fees after controlling for auditor quality and other factors that affect audit fees, suggesting that stock return asynchronicity is more likely to capture a company's firm-specific information than its information environment. We also find that asynchronous firms are more likely to receive adverse opinions on their internal controls over financial reporting, but are associated with lower costs of capital and auditor litigation, providing further evidence in support of the firm-specific information argument. Asynchronicity's positive association with audit fees is driven by firms with higher accounting reporting complexity, suggesting stock return asynchronicity captures a firm's complexity, resulting in more significant efforts by the auditor.

Can Mentoring Alleviate Family Disadvantage in Adolescence? A Field Experiment to Improve Labor-Market Prospects

Sven Resnjanskij

Jens Ruhose

Simon Wiederhold

Ludger Woessmann

Katharina Wedel

in: Journal of Political Economy,

forthcoming

Abstract

We study a mentoring program that aims to improve the labor-market prospects of school-attending adolescents from disadvantaged families by offering them a university-student mentor. Our RCT investigates program effectiveness on three outcome dimensions that are highly predictive of later labor-market success: math grades, patience/social skills, and labor-market orientation. For low-SES adolescents, the mentoring increases a combined index of the outcomes by over half a standard deviation after one year, with significant increases in each dimension. Part of the treatment effect is mediated by establishing mentors as attachment figures who provide guidance for the future. Effects on grades and labor-market orientation, but not on patience/social skills, persist three years after program start. By that time, the mentoring also improves early realizations of school-to-work transitions for low-SES adolescents. The mentoring is not effective for higher-SES adolescents. The results show that substituting lacking family support by other adults can help disadvantaged children at adolescent age.

in: Journal of Financial and Quantitative Analysis,

forthcoming

Abstract

This study examines how antitrust law adoptions affect horizontal merger and acquisition (M&A) outcomes. Using the staggered introduction of competition laws in 20 countries, we find antitrust regulation decreases acquirers’ five-day cumulative abnormal returns surrounding horizontal merger announcements. A decrease in deal value, target book assets, and industry peers' announcement returns are consistent with the market power hypothesis. Exploiting antitrust law adoptions addresses a downward bias to an estimated effect of antitrust enforcement (Baker (2003)). The potential bias from heterogeneous treatment effects does not nullify our results. Overall, antitrust policies seem to deter post-merger monopolistic gains, potentially improving customer welfare.

in: Review of Corporate Finance Studies,

forthcoming

Abstract

We analyze how creditor rights affect the nonsynchronicity of global corporate credit default swap spreads (CDS-NS). CDS-NS is negatively related to the country-level creditor-control rights, especially to the “restrictions on reorganization” component, where creditor-shareholder conflicts are high. The effect is concentrated in firms with high investment intensity, asset growth, information opacity, and risk. Pro-creditor bankruptcy reforms led to a decline in CDS-NS, indicating lower firm-specific idiosyncratic information being priced in credit markets. A strategic-disclosure incentive among debtors avoiding creditor intervention seems more dominant than the disciplining effect, suggesting how strengthening creditor rights affects power rebalancing between creditors and shareholders.

Considering the inherent stickiness of abnormal audit fees, our study contributes to the literature by decomposing abnormal audit fees into a jump component and long-run sticky component. We investigate whether and how changes in credit ratings asymmetrically affect the jump component of abnormal audit fees. We document a positive association between rating downgrades and the jump component. We find that heightened bankruptcy risk and misstatement risk are the mechanisms that drive this relationship. Further analysis shows that firms experiencing rating downgrades are more likely to receive a going concern opinion and experience longer audit report lags. Taken together, our findings provide direct evidence that credit ratings are significantly associated with abnormal audit fees, particularly with the jump component. Given the serial correlation of abnormal audit fees, our study sheds light on the importance of disaggregation of the abnormal audit fee residuals into the jump and long-run sticky components.

in: Review of Economics and Statistics,

forthcoming

Abstract

Why do cities differ so much in productivity? A long literature has sought out systematic sources, such as inherent productivity advantages, market access, agglomeration forces, or sorting. We document that up to three quarters of the measured regional productivity dispersion is spurious, reflecting the “luck of the draw” of finite counts of idiosyncratically heterogeneous plants that happen to operate in a given location. The patterns are even more pronounced for new plants, hold for alternative productivity measures, and broadly extend to European countries. This large role for individual plants suggests a smaller role for places in driving regional differences.

in: Journal of Money, Credit and Banking,

forthcoming

Abstract

Abstract This paper investigates the relationship between heterogeneity in sectoral price stickiness and the response of the economy to aggregate real shocks. We show that sectoral heterogeneity reduces inflation persistence for a constant average duration of price spells, and that inflation persistence can fall despite duration increases associated with increases in heterogeneity. We also find that sectoral heterogeneity reduces the persistence and volatility of interest rate and output gap for a constant price spells duration, while the qualitative impact on inflation volatility tends to be positive. A relevant policy implication is that neglecting price stickiness heterogeneity can impair the economic dynamics assessment.

in: Journal of Financial and Quantitative Analysis,

forthcoming

Abstract

Mutual fund families increasingly hold bonds and stocks from the same firm. We present evidence that dual ownership allows firms to increase valuable investments and refinance by issuing bonds with lower yields and fewer restrictive covenants, especially when firms face financial distress. Dual holders also prevent overinvestment by firms with entrenched managers. Overall, our results suggest that mutual fund families internalize the agency conflicts of their portfolio companies, highlighting the positive governance externalities of intra-family cooperation.

in: Jahrbücher für Nationalökonomie und Statistik,

forthcoming

Abstract

Using a newly collected dataset at the plant level from 2014 to 2018, we provide the first microscopic portrait of robotization in Germany and study the correlates of robot adoption. Our descriptive analysis uncovers five stylized facts: (1) Robot use is relatively rare. (2) The distribution of robots is highly skewed. (3) New robot adopters contribute substantially to the recent robotization. (4) Robot users are exceptional. (5) Heterogeneity in robot types matters. Our regression results further suggest plant size, high-skilled labor share, exporter status, and labor shortage to be strongly associated with the future probability of robot adoption.

in: Journal of Business Finance and Accounting,

forthcoming

Abstract

Abstract This paper investigates how state ownership affects financial reporting practices in China. Using several measures of state (government) ownership, we show that a one-standard-deviation increase in state ownership decreases financial statement comparability by 36.61%, and the impact is more pronounced when the central authority has majority control of the company. Moreover, lower earnings quality and lower levels of accounting conservatism among state-owned enterprises (SOEs) may explain the lower accounting comparability between SOEs and non-SOEs (NSOEs). Additionally, similar (different) managerial objectives converge (diverge) financial statement comparability between SOEs and NSOEs. Last, the geographical locations of firms also contribute to financial statement comparability. We employ a difference-in-differences design, changes regression and entropy balancing to mitigate potential endogeneity bias.

in: Journal of Business Finance and Accounting,

forthcoming

Abstract

Abstract This paper investigates a firm's stock return asynchronicity through the auditor's perspective to distinguish whether this asynchronicity can proxy for the company's firm-specific information or the quality of its information environment. We find a significant and positive association between asynchronicity and audit fees after controlling for auditor quality and other factors that affect audit fees, suggesting that stock return asynchronicity is more likely to capture a company's firm-specific information than its information environment. We also find that asynchronous firms are more likely to receive adverse opinions on their internal controls over financial reporting, but are associated with lower costs of capital and auditor litigation, providing further evidence in support of the firm-specific information argument. Asynchronicity's positive association with audit fees is driven by firms with higher accounting reporting complexity, suggesting stock return asynchronicity captures a firm's complexity, resulting in more significant efforts by the auditor.

Can Mentoring Alleviate Family Disadvantage in Adolescence? A Field Experiment to Improve Labor-Market Prospects

Sven Resnjanskij

Jens Ruhose

Simon Wiederhold

Ludger Woessmann

Katharina Wedel

in: Journal of Political Economy,

forthcoming

Abstract

We study a mentoring program that aims to improve the labor-market prospects of school-attending adolescents from disadvantaged families by offering them a university-student mentor. Our RCT investigates program effectiveness on three outcome dimensions that are highly predictive of later labor-market success: math grades, patience/social skills, and labor-market orientation. For low-SES adolescents, the mentoring increases a combined index of the outcomes by over half a standard deviation after one year, with significant increases in each dimension. Part of the treatment effect is mediated by establishing mentors as attachment figures who provide guidance for the future. Effects on grades and labor-market orientation, but not on patience/social skills, persist three years after program start. By that time, the mentoring also improves early realizations of school-to-work transitions for low-SES adolescents. The mentoring is not effective for higher-SES adolescents. The results show that substituting lacking family support by other adults can help disadvantaged children at adolescent age.

in: Journal of Financial and Quantitative Analysis,

forthcoming

Abstract

This study examines how antitrust law adoptions affect horizontal merger and acquisition (M&A) outcomes. Using the staggered introduction of competition laws in 20 countries, we find antitrust regulation decreases acquirers’ five-day cumulative abnormal returns surrounding horizontal merger announcements. A decrease in deal value, target book assets, and industry peers' announcement returns are consistent with the market power hypothesis. Exploiting antitrust law adoptions addresses a downward bias to an estimated effect of antitrust enforcement (Baker (2003)). The potential bias from heterogeneous treatment effects does not nullify our results. Overall, antitrust policies seem to deter post-merger monopolistic gains, potentially improving customer welfare.

in: Review of Corporate Finance Studies,

forthcoming

Abstract

We analyze how creditor rights affect the nonsynchronicity of global corporate credit default swap spreads (CDS-NS). CDS-NS is negatively related to the country-level creditor-control rights, especially to the “restrictions on reorganization” component, where creditor-shareholder conflicts are high. The effect is concentrated in firms with high investment intensity, asset growth, information opacity, and risk. Pro-creditor bankruptcy reforms led to a decline in CDS-NS, indicating lower firm-specific idiosyncratic information being priced in credit markets. A strategic-disclosure incentive among debtors avoiding creditor intervention seems more dominant than the disciplining effect, suggesting how strengthening creditor rights affects power rebalancing between creditors and shareholders.

Considering the inherent stickiness of abnormal audit fees, our study contributes to the literature by decomposing abnormal audit fees into a jump component and long-run sticky component. We investigate whether and how changes in credit ratings asymmetrically affect the jump component of abnormal audit fees. We document a positive association between rating downgrades and the jump component. We find that heightened bankruptcy risk and misstatement risk are the mechanisms that drive this relationship. Further analysis shows that firms experiencing rating downgrades are more likely to receive a going concern opinion and experience longer audit report lags. Taken together, our findings provide direct evidence that credit ratings are significantly associated with abnormal audit fees, particularly with the jump component. Given the serial correlation of abnormal audit fees, our study sheds light on the importance of disaggregation of the abnormal audit fee residuals into the jump and long-run sticky components.

in: Review of Economics and Statistics,

forthcoming

Abstract

Why do cities differ so much in productivity? A long literature has sought out systematic sources, such as inherent productivity advantages, market access, agglomeration forces, or sorting. We document that up to three quarters of the measured regional productivity dispersion is spurious, reflecting the “luck of the draw” of finite counts of idiosyncratically heterogeneous plants that happen to operate in a given location. The patterns are even more pronounced for new plants, hold for alternative productivity measures, and broadly extend to European countries. This large role for individual plants suggests a smaller role for places in driving regional differences.

in: Journal of Money, Credit and Banking,

forthcoming

Abstract

Abstract This paper investigates the relationship between heterogeneity in sectoral price stickiness and the response of the economy to aggregate real shocks. We show that sectoral heterogeneity reduces inflation persistence for a constant average duration of price spells, and that inflation persistence can fall despite duration increases associated with increases in heterogeneity. We also find that sectoral heterogeneity reduces the persistence and volatility of interest rate and output gap for a constant price spells duration, while the qualitative impact on inflation volatility tends to be positive. A relevant policy implication is that neglecting price stickiness heterogeneity can impair the economic dynamics assessment.

in: Journal of Financial and Quantitative Analysis,

forthcoming

Abstract

Mutual fund families increasingly hold bonds and stocks from the same firm. We present evidence that dual ownership allows firms to increase valuable investments and refinance by issuing bonds with lower yields and fewer restrictive covenants, especially when firms face financial distress. Dual holders also prevent overinvestment by firms with entrenched managers. Overall, our results suggest that mutual fund families internalize the agency conflicts of their portfolio companies, highlighting the positive governance externalities of intra-family cooperation.

in: Jahrbücher für Nationalökonomie und Statistik,

forthcoming

Abstract

Using a newly collected dataset at the plant level from 2014 to 2018, we provide the first microscopic portrait of robotization in Germany and study the correlates of robot adoption. Our descriptive analysis uncovers five stylized facts: (1) Robot use is relatively rare. (2) The distribution of robots is highly skewed. (3) New robot adopters contribute substantially to the recent robotization. (4) Robot users are exceptional. (5) Heterogeneity in robot types matters. Our regression results further suggest plant size, high-skilled labor share, exporter status, and labor shortage to be strongly associated with the future probability of robot adoption.

in: Journal of Business Finance and Accounting,

forthcoming

Abstract

Abstract This paper investigates how state ownership affects financial reporting practices in China. Using several measures of state (government) ownership, we show that a one-standard-deviation increase in state ownership decreases financial statement comparability by 36.61%, and the impact is more pronounced when the central authority has majority control of the company. Moreover, lower earnings quality and lower levels of accounting conservatism among state-owned enterprises (SOEs) may explain the lower accounting comparability between SOEs and non-SOEs (NSOEs). Additionally, similar (different) managerial objectives converge (diverge) financial statement comparability between SOEs and NSOEs. Last, the geographical locations of firms also contribute to financial statement comparability. We employ a difference-in-differences design, changes regression and entropy balancing to mitigate potential endogeneity bias.

in: Journal of Business Finance and Accounting,

forthcoming

Abstract

Abstract This paper investigates a firm's stock return asynchronicity through the auditor's perspective to distinguish whether this asynchronicity can proxy for the company's firm-specific information or the quality of its information environment. We find a significant and positive association between asynchronicity and audit fees after controlling for auditor quality and other factors that affect audit fees, suggesting that stock return asynchronicity is more likely to capture a company's firm-specific information than its information environment. We also find that asynchronous firms are more likely to receive adverse opinions on their internal controls over financial reporting, but are associated with lower costs of capital and auditor litigation, providing further evidence in support of the firm-specific information argument. Asynchronicity's positive association with audit fees is driven by firms with higher accounting reporting complexity, suggesting stock return asynchronicity captures a firm's complexity, resulting in more significant efforts by the auditor.

Can Mentoring Alleviate Family Disadvantage in Adolescence? A Field Experiment to Improve Labor-Market Prospects

Sven Resnjanskij

Jens Ruhose

Simon Wiederhold

Ludger Woessmann

Katharina Wedel

in: Journal of Political Economy,

forthcoming

Abstract

We study a mentoring program that aims to improve the labor-market prospects of school-attending adolescents from disadvantaged families by offering them a university-student mentor. Our RCT investigates program effectiveness on three outcome dimensions that are highly predictive of later labor-market success: math grades, patience/social skills, and labor-market orientation. For low-SES adolescents, the mentoring increases a combined index of the outcomes by over half a standard deviation after one year, with significant increases in each dimension. Part of the treatment effect is mediated by establishing mentors as attachment figures who provide guidance for the future. Effects on grades and labor-market orientation, but not on patience/social skills, persist three years after program start. By that time, the mentoring also improves early realizations of school-to-work transitions for low-SES adolescents. The mentoring is not effective for higher-SES adolescents. The results show that substituting lacking family support by other adults can help disadvantaged children at adolescent age.

in: Journal of Financial and Quantitative Analysis,

forthcoming

Abstract

This study examines how antitrust law adoptions affect horizontal merger and acquisition (M&A) outcomes. Using the staggered introduction of competition laws in 20 countries, we find antitrust regulation decreases acquirers’ five-day cumulative abnormal returns surrounding horizontal merger announcements. A decrease in deal value, target book assets, and industry peers' announcement returns are consistent with the market power hypothesis. Exploiting antitrust law adoptions addresses a downward bias to an estimated effect of antitrust enforcement (Baker (2003)). The potential bias from heterogeneous treatment effects does not nullify our results. Overall, antitrust policies seem to deter post-merger monopolistic gains, potentially improving customer welfare.

in: Review of Corporate Finance Studies,

forthcoming

Abstract

We analyze how creditor rights affect the nonsynchronicity of global corporate credit default swap spreads (CDS-NS). CDS-NS is negatively related to the country-level creditor-control rights, especially to the “restrictions on reorganization” component, where creditor-shareholder conflicts are high. The effect is concentrated in firms with high investment intensity, asset growth, information opacity, and risk. Pro-creditor bankruptcy reforms led to a decline in CDS-NS, indicating lower firm-specific idiosyncratic information being priced in credit markets. A strategic-disclosure incentive among debtors avoiding creditor intervention seems more dominant than the disciplining effect, suggesting how strengthening creditor rights affects power rebalancing between creditors and shareholders.

Considering the inherent stickiness of abnormal audit fees, our study contributes to the literature by decomposing abnormal audit fees into a jump component and long-run sticky component. We investigate whether and how changes in credit ratings asymmetrically affect the jump component of abnormal audit fees. We document a positive association between rating downgrades and the jump component. We find that heightened bankruptcy risk and misstatement risk are the mechanisms that drive this relationship. Further analysis shows that firms experiencing rating downgrades are more likely to receive a going concern opinion and experience longer audit report lags. Taken together, our findings provide direct evidence that credit ratings are significantly associated with abnormal audit fees, particularly with the jump component. Given the serial correlation of abnormal audit fees, our study sheds light on the importance of disaggregation of the abnormal audit fee residuals into the jump and long-run sticky components.

in: Review of Economics and Statistics,

forthcoming

Abstract

Why do cities differ so much in productivity? A long literature has sought out systematic sources, such as inherent productivity advantages, market access, agglomeration forces, or sorting. We document that up to three quarters of the measured regional productivity dispersion is spurious, reflecting the “luck of the draw” of finite counts of idiosyncratically heterogeneous plants that happen to operate in a given location. The patterns are even more pronounced for new plants, hold for alternative productivity measures, and broadly extend to European countries. This large role for individual plants suggests a smaller role for places in driving regional differences.

in: Journal of Money, Credit and Banking,

forthcoming

Abstract

Abstract This paper investigates the relationship between heterogeneity in sectoral price stickiness and the response of the economy to aggregate real shocks. We show that sectoral heterogeneity reduces inflation persistence for a constant average duration of price spells, and that inflation persistence can fall despite duration increases associated with increases in heterogeneity. We also find that sectoral heterogeneity reduces the persistence and volatility of interest rate and output gap for a constant price spells duration, while the qualitative impact on inflation volatility tends to be positive. A relevant policy implication is that neglecting price stickiness heterogeneity can impair the economic dynamics assessment.

in: Journal of Financial and Quantitative Analysis,

forthcoming

Abstract

Mutual fund families increasingly hold bonds and stocks from the same firm. We present evidence that dual ownership allows firms to increase valuable investments and refinance by issuing bonds with lower yields and fewer restrictive covenants, especially when firms face financial distress. Dual holders also prevent overinvestment by firms with entrenched managers. Overall, our results suggest that mutual fund families internalize the agency conflicts of their portfolio companies, highlighting the positive governance externalities of intra-family cooperation.

in: Jahrbücher für Nationalökonomie und Statistik,

forthcoming

Abstract

Using a newly collected dataset at the plant level from 2014 to 2018, we provide the first microscopic portrait of robotization in Germany and study the correlates of robot adoption. Our descriptive analysis uncovers five stylized facts: (1) Robot use is relatively rare. (2) The distribution of robots is highly skewed. (3) New robot adopters contribute substantially to the recent robotization. (4) Robot users are exceptional. (5) Heterogeneity in robot types matters. Our regression results further suggest plant size, high-skilled labor share, exporter status, and labor shortage to be strongly associated with the future probability of robot adoption.

in: Journal of Business Finance and Accounting,

forthcoming

Abstract

Abstract This paper investigates how state ownership affects financial reporting practices in China. Using several measures of state (government) ownership, we show that a one-standard-deviation increase in state ownership decreases financial statement comparability by 36.61%, and the impact is more pronounced when the central authority has majority control of the company. Moreover, lower earnings quality and lower levels of accounting conservatism among state-owned enterprises (SOEs) may explain the lower accounting comparability between SOEs and non-SOEs (NSOEs). Additionally, similar (different) managerial objectives converge (diverge) financial statement comparability between SOEs and NSOEs. Last, the geographical locations of firms also contribute to financial statement comparability. We employ a difference-in-differences design, changes regression and entropy balancing to mitigate potential endogeneity bias.

in: Journal of Business Finance and Accounting,

forthcoming

Abstract

Abstract This paper investigates a firm's stock return asynchronicity through the auditor's perspective to distinguish whether this asynchronicity can proxy for the company's firm-specific information or the quality of its information environment. We find a significant and positive association between asynchronicity and audit fees after controlling for auditor quality and other factors that affect audit fees, suggesting that stock return asynchronicity is more likely to capture a company's firm-specific information than its information environment. We also find that asynchronous firms are more likely to receive adverse opinions on their internal controls over financial reporting, but are associated with lower costs of capital and auditor litigation, providing further evidence in support of the firm-specific information argument. Asynchronicity's positive association with audit fees is driven by firms with higher accounting reporting complexity, suggesting stock return asynchronicity captures a firm's complexity, resulting in more significant efforts by the auditor.

Can Mentoring Alleviate Family Disadvantage in Adolescence? A Field Experiment to Improve Labor-Market Prospects

Sven Resnjanskij

Jens Ruhose

Simon Wiederhold

Ludger Woessmann

Katharina Wedel

in: Journal of Political Economy,

forthcoming

Abstract

We study a mentoring program that aims to improve the labor-market prospects of school-attending adolescents from disadvantaged families by offering them a university-student mentor. Our RCT investigates program effectiveness on three outcome dimensions that are highly predictive of later labor-market success: math grades, patience/social skills, and labor-market orientation. For low-SES adolescents, the mentoring increases a combined index of the outcomes by over half a standard deviation after one year, with significant increases in each dimension. Part of the treatment effect is mediated by establishing mentors as attachment figures who provide guidance for the future. Effects on grades and labor-market orientation, but not on patience/social skills, persist three years after program start. By that time, the mentoring also improves early realizations of school-to-work transitions for low-SES adolescents. The mentoring is not effective for higher-SES adolescents. The results show that substituting lacking family support by other adults can help disadvantaged children at adolescent age.

in: Journal of Financial and Quantitative Analysis,

forthcoming

Abstract

This study examines how antitrust law adoptions affect horizontal merger and acquisition (M&A) outcomes. Using the staggered introduction of competition laws in 20 countries, we find antitrust regulation decreases acquirers’ five-day cumulative abnormal returns surrounding horizontal merger announcements. A decrease in deal value, target book assets, and industry peers' announcement returns are consistent with the market power hypothesis. Exploiting antitrust law adoptions addresses a downward bias to an estimated effect of antitrust enforcement (Baker (2003)). The potential bias from heterogeneous treatment effects does not nullify our results. Overall, antitrust policies seem to deter post-merger monopolistic gains, potentially improving customer welfare.

in: Review of Corporate Finance Studies,

forthcoming

Abstract

We analyze how creditor rights affect the nonsynchronicity of global corporate credit default swap spreads (CDS-NS). CDS-NS is negatively related to the country-level creditor-control rights, especially to the “restrictions on reorganization” component, where creditor-shareholder conflicts are high. The effect is concentrated in firms with high investment intensity, asset growth, information opacity, and risk. Pro-creditor bankruptcy reforms led to a decline in CDS-NS, indicating lower firm-specific idiosyncratic information being priced in credit markets. A strategic-disclosure incentive among debtors avoiding creditor intervention seems more dominant than the disciplining effect, suggesting how strengthening creditor rights affects power rebalancing between creditors and shareholders.

Considering the inherent stickiness of abnormal audit fees, our study contributes to the literature by decomposing abnormal audit fees into a jump component and long-run sticky component. We investigate whether and how changes in credit ratings asymmetrically affect the jump component of abnormal audit fees. We document a positive association between rating downgrades and the jump component. We find that heightened bankruptcy risk and misstatement risk are the mechanisms that drive this relationship. Further analysis shows that firms experiencing rating downgrades are more likely to receive a going concern opinion and experience longer audit report lags. Taken together, our findings provide direct evidence that credit ratings are significantly associated with abnormal audit fees, particularly with the jump component. Given the serial correlation of abnormal audit fees, our study sheds light on the importance of disaggregation of the abnormal audit fee residuals into the jump and long-run sticky components.

in: Review of Economics and Statistics,

forthcoming

Abstract

Why do cities differ so much in productivity? A long literature has sought out systematic sources, such as inherent productivity advantages, market access, agglomeration forces, or sorting. We document that up to three quarters of the measured regional productivity dispersion is spurious, reflecting the “luck of the draw” of finite counts of idiosyncratically heterogeneous plants that happen to operate in a given location. The patterns are even more pronounced for new plants, hold for alternative productivity measures, and broadly extend to European countries. This large role for individual plants suggests a smaller role for places in driving regional differences.

Joint Economic Forecast Spring 2024: Headwinds from Germany and abroad: institutes revise forecast significantly downwards

According to Germany’s five leading economic research institutes, the country’s economy shows cyclical and structural weaknesses. In their spring report, they revised their GDP forecast for the current year significantly downward to 0.1%. In the recent fall report, the figure was still 1.3%. Expectations for the coming year are almost unchanged at 1.4% (previously 1.5%). However, the level of economic activity will then be over 30 billion euros lower due to the current weak phase.

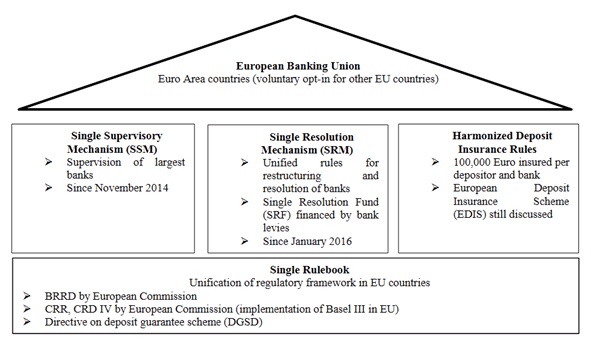

New Regulatory Framework in Europe

This figure shows the different pillars that form the basis of the new regulatory framework in Europe. The Single Rulebook applies to all 28 member states. The three pillars of the European Banking Union are obligatory for Euro Area countries and voluntary for the remaining EU member states.

Source: Koetter, Michael; Krause, Thomas; Tonzer, Lena (2017): Delay determinants of European Banking Union implementation. IWH Discussion Papers 24/2017, Halle Institute for Economic Research (IWH).

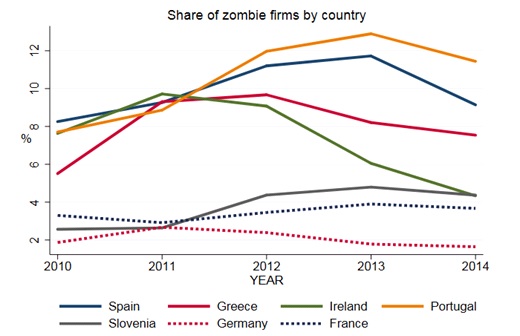

Share of Zombie Firms 2010-2014 by Country

The graph shows the percentage share of firms that have been classified as zombies in a given year and country. Zombie firms are firms, that for at least two consecutive years have negative returns, negative investment, and debt servicing capacity (EBITDA/ financial debt) below 5 %.

Source: Koetter, Michael; Setzer, Ralph; Storz, Manuela; Westphal, Andreas (2017): Do we want these two to tango? On zombie firms and stressed banks in Europe. IWH Discussion Papers 13/2017, Halle Institute for Economic Research (IWH).

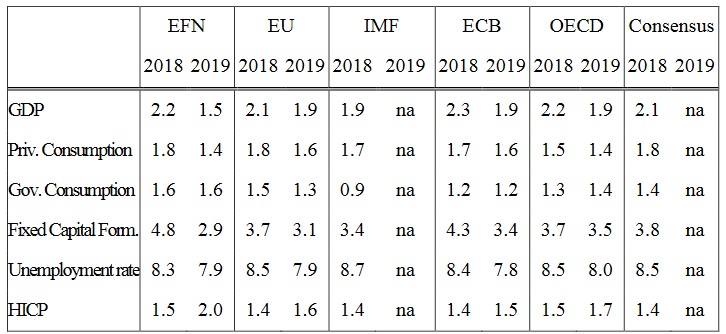

Comparison of EFN Forecasts with Alternative Forecasts

EU: European Commission, Economic Forecast, November 2017; IMF: World Economic Outlook, October 2017, ECB: December 2017 staff macroeconomic projections. OECD: Economic Outlook, November 2017; Consensus: Consensus Economics, Consensus Forecasts, December 2017.

Source: EFN-European Forecasting Network (2017): EFN Report: Economic Outlook for the Euro Area in 2018 and 2019.

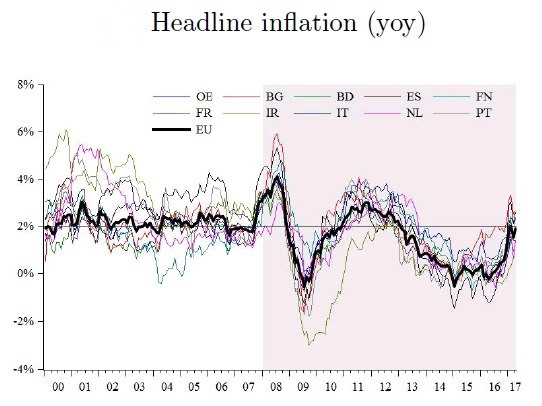

Euro Area Inflation Dynamics and Possible Drivers (a)

This figure (a) shows headline inflation rates in the Euro area and in ten member countries of the European Monetary Union (EMU). The possible inflation drivers may all have contributed to the low inflation rate in recent years. The series of survey- and market-based inflation expectations were obtained from Consensus Economics, Thomson Reuters and own calculations. For the remaining data sources it is referred to the data and estimation section.

Source: Dany-Knedlik, Geraldine; Holtemöller, Oliver (2017): Inflation dynamics during the financial crisis in Europe: Cross-sectional identification of long-run inflation expectations. IWH Discussion Papers 10/2017, Halle Institute for Economic Research (IWH).

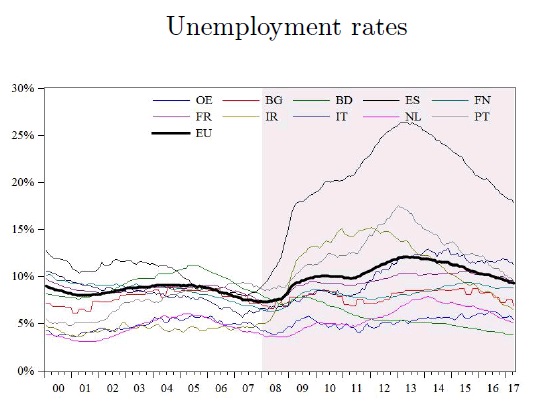

Euro Area Inflation Dynamics and Possible Drivers (b)

This figure (b) shows unemployment rates in the Euro area and in ten member countries of the European Monetary Union (EMU). The possible inflation drivers may all have contributed to the low inflation rate in recent years. The series of survey- and market-based inflation expectations were obtained from Consensus Economics, Thomson Reuters and own calculations. For the remaining data sources it is referred to the data and estimation section.

Source: Dany-Knedlik, Geraldine; Holtemöller, Oliver (2017): Inflation dynamics during the financial crisis in Europe: Cross-sectional identification of long-run inflation expectations. IWH Discussion Papers 10/2017, Halle Institute for Economic Research (IWH).

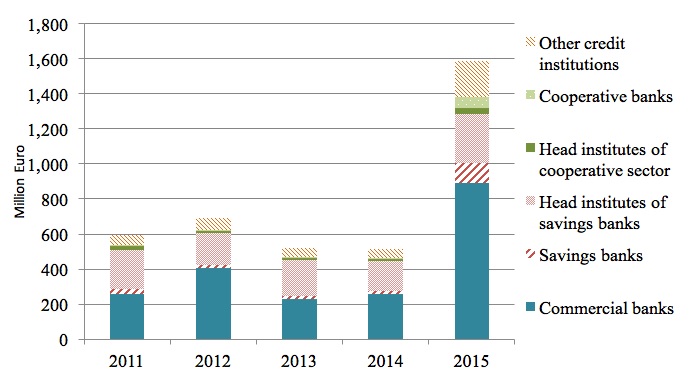

Bank Levies Paid by German Banks

This figure shows the payments of the bank levy (in million euros) by German banks for the years 2011-2015, broken down by banking group. During the years 2011-2014, banks had to contribute to the national restructuring fund as specified in the Restructuring Fund Act. In 2015, banks contributions were for the first time calculated as specified in the Banking Resolution and Restructuring Directive.

Source of Figure: Deutscher Bundestag Drucksache 18/5993, BB8/5993he 18 5 December 2015.

Source: Buch, Claudia; Tonzer, Lena; Weigert, Benjamin (2017): Assessing the effects of regulatory bank levies. VOX CEPR's Policy Portal: Research-based policy analysis and commentary from leading economists.

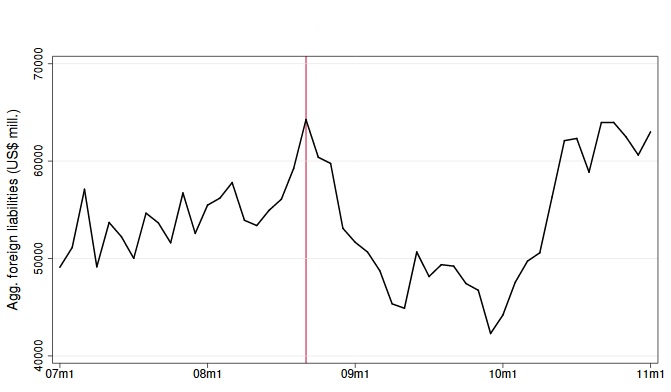

Aggregated Foreign Funding for Brazilian Banks (2007-2010)

This figure shows the development of aggregated foreign funding for Brazilian banks between January 2007 and December 2010. The vertical line is set at September 2008, the month when the collapse of Lehman Brothers triggered a freeze in global interbank markets. Foreign funding is aggregated from the bank-level data in the baseline sample. The variable is reported in real 2013 US$ millions.

Source: Noth, Felix; Ossandon Busch, Matias (2017): Banking globalization, local lending, and labor market effects: Micro-level evidence from Brazil. IWH Discussion Papers 7/2017, Halle Institute for Economic Research (IWH).

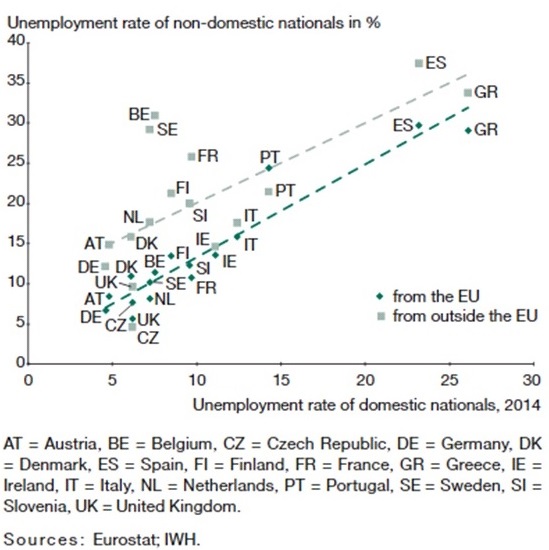

Unemployment Rates by Nationality (2014)

The unemployment rate of EU nationals in most countries is slightly higher than that of domestic nationals; these rates are almost perfectly correlated for all member states. As the figure displays, the unemployment rate of citizens from non-EU member states is significantly higher than that of domestic nationals in almost all countries; the dispersion of the rates is also significantly greater.

Source: Altemeyer-Bartscher, Martin; Holtemöller, Oliver; Lindner, Axel; Schmalzbauer, Andreas; Zeddies, Götz (2016): On the Distribution of Refugees in the EU. In: Intereconomics, Volume 51, July/August 2016, Number 4, pp. 220-228.

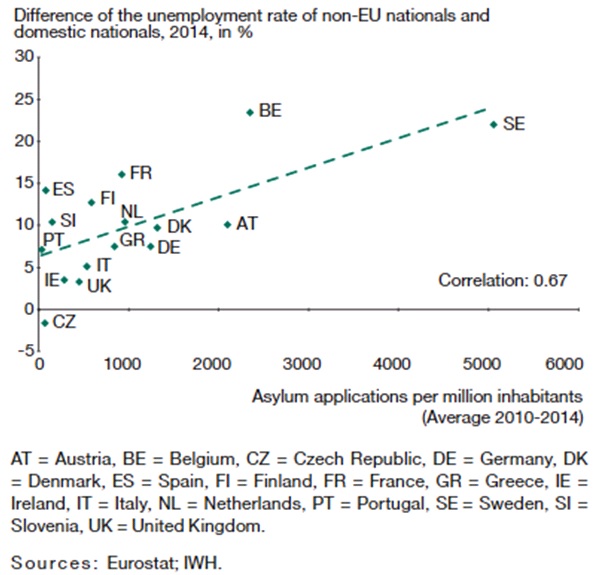

Labour Market Situation for Non-EU Foreigners in Relation to the Number of Applications for Asylum (2014)

In fact, there is a positive correlation between the number of applications for asylum in recent years and the difference in the unemployment rates of domestic nationals and of citizens from non-EU member states (as shown in the figure at hand). This indicates that the marginal costs of integrating refugees do indeed increase as the number of refugees grows.

Source: Altemeyer-Bartscher, Martin; Holtemöller, Oliver; Lindner, Axel; Schmalzbauer, Andreas; Zeddies, Götz (2016): On the Distribution of Refugees in the EU. In: Intereconomics, Volume 51, July/August 2016, Number 4, pp. 220-228.

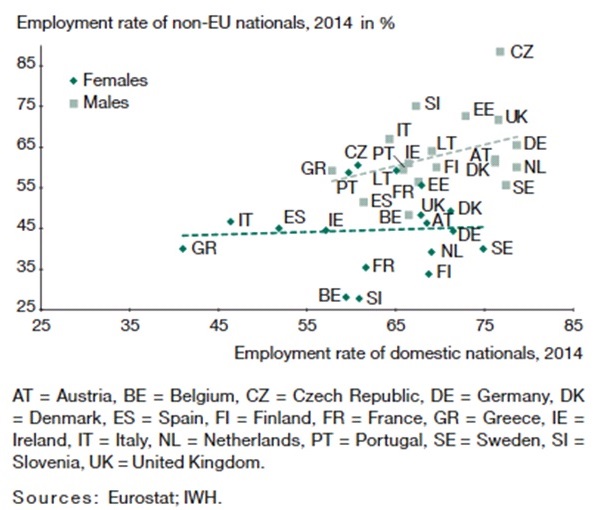

Employment Rates by Nationality and Gender (2014)

Large differences between nationals and foreigners from non-EU countries can also be observed when it comes to the employment rate. In most countries, the employment rate is considerably lower for non-EU citizens than for domestic nationals; this is the case especially for women, but it applies to men as well. While the employment rate of male non-EU foreigners increases at least somewhat with the employment rate of male domestic nationals, the employment rate of female non-EU foreigners is largely disconnected from the domestic rate (see figure above).

Source: Altemeyer-Bartscher, Martin; Holtemöller, Oliver; Lindner, Axel; Schmalzbauer, Andreas; Zeddies, Götz (2016): On the Distribution of Refugees in the EU. In: Intereconomics, Volume 51, July/August 2016, Number 4, pp. 220-228.

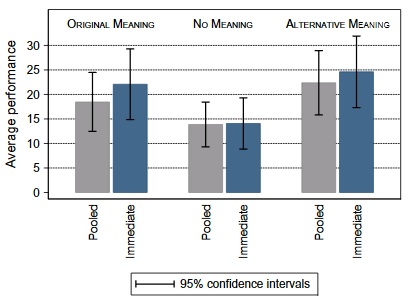

Average Work Performance of Employees Based on Meaning of Task (2014)

The figure demonstrates that the average number of responses differs between the three treatment groups "Original Meaning", "No Meaning" and "Alternative Meaning". It shows the average work performance of workers fulfilling the same task with the same reward but with different information about the usefulness or meaning of their work done before.

Since some workers did not respond at first and only participated in the experiment as latecomers after they were sent further invitations, these were considered as a special group. Therefore, two different groups were created "Immediate" and "Pooled" and were considered separately. In essence, the additional "Pooled" group consists of latecomers grouped together with the employees that immediately participated in the experiment.

Source: Chadi, Adrian; Jeworrek, Sabrina; Mertins, Vanessa (2016): When the Meaning of Work Has Disappeared: Experimental Evidence on Employees’ Performance and Emotions. Management Science 63(6): 1696-1707.